The FinTech Payment Story

Posted by | Alok Tayal

Robert H. Goddard, the father of modern rocket propulsion said, “It is difficult to say what is impossible, for the dream of yesterday is the hope of today and the reality of tomorrow.” Thanks to FinTech, from peer-to-peer lending to being rewarded for making our bill payments on time, the dream of a global cashless economy is more realistic than ever.

Until now, financial institutions offered only traditional services, such as banking activities and trading facilities. However, when conventional finance converges with technology, it unleashes vast opportunities. in In January 2021 cryptocurrencies saw Bitcoin’s daily transactions exceed 400,000 for the first time, and the rise of online platforms has enabled digital lending from businesses such as Affirm and SoFi, trading/investing services from businesses such as Acorns and Robinhood, and crowdfunding from platforms including Patreon, Gracenote, and Kickstarter, which enable artists and founders to raise funds. Crowd financing renewable energy projects in Austria and Switzerland are also a huge milestone.

Online Payments: The jewel in the FinTech Crown

The online payment segment has evolved to become a prominent part of the FinTech establishment. Elon Musk’s Paypal started in the 90s, but it wasn’t until the last decade that we saw any tremendous progress. Now, we have numerous platforms and apps alongside Paypal that are driving the cashless revolution, including Venmo, Zelle, Square, Stripe.

In 2020, the market size for global digital payments was estimated to be $5.4tr and is expected to grow at an 11.2% CAGR, reaching a staggering $11.3tr by 2026. Reflecting this data, in 2020 over 70.3 billion real-time online transactions were made globally – 41% growth YoY, which is likely to increase to ~$6,682,332m in 2022, and projected to reach $10,517,932m by 2025. This amount of money changing hands so quickly and effortlessly reinforces the potential for the sector, whether for grocery stores or venture capitalists, thus encouraging many start-ups to accelerate their growth, with funding pouring in to change how people transact forever.

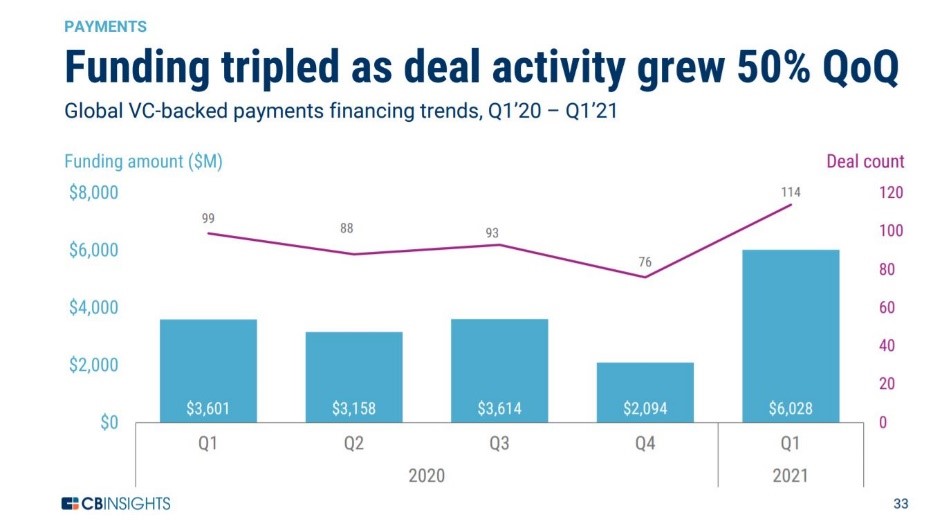

The big shot of online payment: PV & VC Funding

With COVID-19, businesses around the globe suffered, but for the online payment segment it was a game-changer, seeing, in the second half of 2020, an influx of PEVC money into the FinTech space. Robinhood raised $1.3bn via two funding rounds, Klarna – a Sweden-based digital bank – raised $650m, and Chime & Revolut managed to secure investments of $533m and $580m respectively from investors such as Ribbit Capital, Sequoia, and Index Ventures. To the right is a snapshot of payment FinTech’s funding growth for the period of 2020-2021:

In Q1 of 2021, VC firm Tiger Global invested heavily in payment FinTech, including deals such as a series C $450m investment in checkout.com, and series D $300m investment in Rapyd. Other big VC names that have invested in 500 digital payment start-ups include Sequoia, Accel, Ribbit Capital. Sequoia Capital invested in over 50 Indian companies in 2020, amounting to $1.35bn, most of which were FinTech giants such as RazorPay and Khatabook.

Other VC-funded payment FinTechs that have raised capital this year include Stripe ($600m), PPRO ($270m), Moss ($25.5m), and Dash ($0.12m). The digital payment company Square Inc. has also secured a $29bn deal and will purchase the Australian buy now, pay later platform Afterpay Limited.

More capital, more growth, more entrants

Accelerated growth and market traction always leads to the threat of new entrants. Hype, the hike in funding rounds, and the overall growth for start-ups in this segment have worked as a hook for attracting new, big fish.

This includes not only financial players but also non-financial, non-banking companies such as Apple Pay and Amazon Pay. Starbucks (via its loyalty programs) and Uber Money are further example of non-banking companies breaking into this vertical. In addition, WhatsApp has formally registered its unconventional entry into the digital payment stream. GooglePay is also among the heavyweight competitors, while PayPal and Square Capital have successfully pivoted their business models, generating billions in profit. And, backed by SoftBank, Southeast Asia’s biggest super app, Grab, also applied for a banking license in Singapore, post-liberalization in 2019.

Becoming brands in the digital payment market, these new entries are ending the traditional cycle and creating a tug of war between them and the old and traditional players already in the field.

Can modern disrupt the traditional?

Before digital payment became prevalent, people carried out their financial transactions through cheques, bankers’ drafts, visiting banks, or cash. However, times have changed, whether buying your morning coffee or a million-dollar investment, everything can now be done at the touch of a finger and from the convenience at your home.

FinTech is giving traditional banking a good run for its money by targeting their market share, margins, information security/privacy, and customer churn in a much more aggressive manner.

The reasons behind this threat are varied. Digital payment disruption has brought innovation in terms of digital currencies and blockchain, and has improved efficiency and supply diversification through faster turnaround times for transactions and access to a range of payment options. But this is not limited to online payments. Other traditional banking activities such as credit lending and advisory services are also feeling the impact.

In addition, the higher rate of competition has increased pressure for conventional players to curb their margins, whether for payments or brokerage services. Top traditional banks such as Bank Of America and JP Morgan have already slated cryptocurrencies as a threat, and PwC, in its 2020 Global FinTech Survey, finds that around 28% of banking and payment businesses, and 22% of insurance, wealth, and asset management companies are facing disruption from FinTech.

Despite this, bankers seem to widely underestimate the threat they are facing. Online payments and digital commerce are becoming increasingly competitive, which banks need to recognize and respond to as a matter of urgency, if they are to safeguard their interests.

Risk components of the FinTech payment sector

There are two major threats for this sector:

1. Peer-to-peer lending and loose regulation

It is believed that without banking charters restraining the sector, online lending platforms can indeed prove to be catastrophic, even for consumers. A good example comes from China’s Peer-to-Peer lending crash, which points to loose regulations triggering foul play, and more recently, the Cajee brothers of South Africa scammed $3.6bn from the users of their CipherTrace Bitcoin platform. Without the appropriate placement of laws or regulations, history can certainly repeat itself.

2. Cyber crime

Like cotton candy stalls at a carnival, FinTech payment companies are prime targets for cybercriminals. The Central Statistics Office (CSO) estimates that in 2021, losses resulting from cyber-attacks are likely to reach $6tr per year, doubling from $3tr in 2015. Data breaches, network security, denial-of-service attacks and the resulting rectification costs, are prime concerns for FinTech companies. Again, systematic risks from cyber terrorists combined with human trafficking, narco-terrorism, and violent attacks can jeopardize all stakeholders.

Despite the risks, the segment is marking its own trajectory with companies penetrating the lesser developed parts of the world along with increasing their presence in the developed countries.

Global shift in online payments

FinTech has also commenced a new era of financial inclusion as previously untouched populations are now benefiting through technology. M-Pesa, launched by the Vodafone group in Kenya, has now expanded to other countries such as Tanzania, South Africa, and even Afghanistan. India’s UPI is also among the prime examples of a highly accessible tech-mediated financial ecosystem.

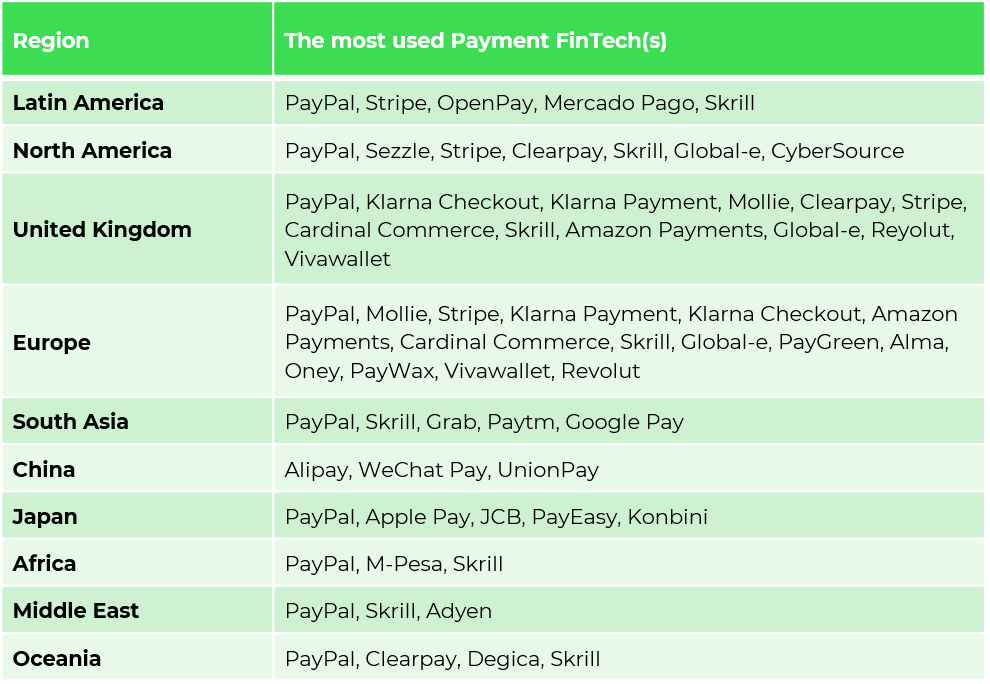

This table shows the digital payment FinTech’s currently dominating regions across the globe:

CyberSource: The Power of Payement: 35 online Payment methods by country, Mercury Minds: Preferred payment methods – countries around the world

FinTech’s expansion into financing solutions

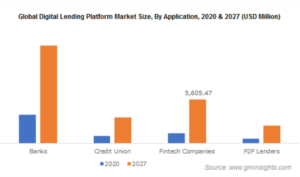

FinTech disruption is not just focused on nations, it has also impacted other financing segments, with lending seeing the biggest impact, and conservative sectors like mortgage lending giving FinTech the Midas touch. Better(.)com is a good example of online mortgage lending platforms revolutionizing an otherwise slow-moving sector. The digital mortgage loan market size is expected to grow to 15% CAGR by 2027.

Online lending is also a big part of digitally-powered payment environments. Companies including Petal, Tala, and Credit Karma are doing exceptionally well in serving credit loans to under-served populations digitally and rapidly. In addition, peer-to-peer lending sites such as Lending Club, Prosper Marketplace, and OnDeck are looking to decrease interest rates by opening up competition for loans to expansive market forces. And business loan companies such as Lendio, Accion, Kabbage, and Funding Circle target start-ups to help them secure working capital and establish their businesses efficiently. At present, the Fed rate is close to zero fuelling the much-needed impetus.

Will the payment FinTech’s story have a bright future?

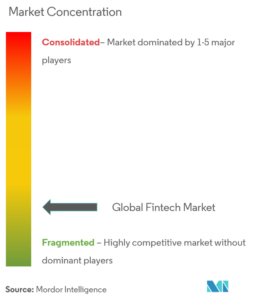

The answer is a yes, without any doubt. The payment FinTech segment is just coming out of its embryo stage, with a lot still to be achieved and explored. The number of players in the digital payments and the FinTech industry overall is substantial, with a few significant players like Ant Financial, Adyen, Xero, SoFi, etc., holding the giant market share. Even so, ample opportunities are yet to be discovered.

The global FinTech market is expected to reach $305.7 bn by 2023, with a 22.17% CAGR from 2018 to 2023. Factors like financial inclusion, FinTech start-ups & funding revolution, and overall usage by the masses are the stars of the show here.

For the new generation that inspires Black Mirror experiences, FinTech could change the way they perceive financial inclusion. Change is the only constant, and with that, the perspective for the FinTech segment looks as promising as social media did a decade ago. All we have to do is wait and watch for this disruption to digitalize the life we once knew!

Tags: Digital Transformation, Financial, Financial Services, Venture Capital