Aetna’s Medicare Advantage Bet

Posted by | Fuld & Company

Last week Aetna announced its intention to acquire Humana for $37 billion in cash and stock. Reasons given for the acquisition included the usual references to synergy potential, cost savings, and greater financial strength, but also how the acquisition will improve membership positioning and increase government exposure in its covered lives portfolio.

These are implicit references to Humana’s Medicare Advantage membership, which according to the Kaiser Family Foundation makes up19% of all Medicare Advantage members – a market share roughly tied for the lead with the country’s largest private payer organizations, United Healthcare. Aetna’s current market share of Medicare Advantage is 7%. The combination of Aetna and Humana creates a Medicare Advantage powerhouse which, given current industry trends, could well be the most significant benefit of this tie-up.

Private Medicare

Medicare Advantage is a private alternative to government managed Fee-For-Services Medicare. Medicare Advantage plans reimburse providers at the same rates as the Centers for Medicare and Medicaid Services, but because Medicare Advantage plans are managed plans, outcomes are better, meaning total costs are lower. In theory the private carriers pass these savings on to members in the form of extra benefits not included in government-run Medicare.

The government subsidizes Medicare Advantage by paying a fixed, per-member amount – adjusted for risk based on the member’s overall health — directly to the plans. These payments were targeted in the ACA for cost reduction with the rate of these payments lowering over time.

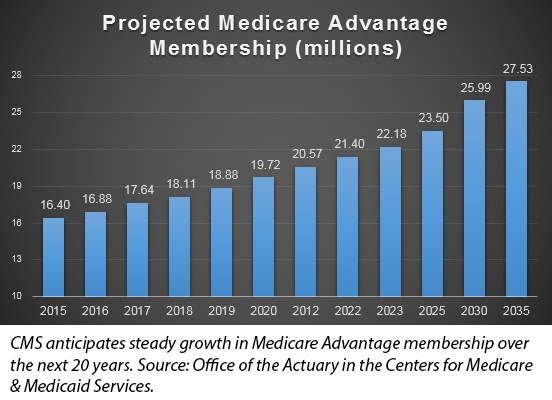

For this reason it was thought Medicare Advantage Membership would decline, but it has instead grown from 11.7 million in 2010 to the current 16.8 million enrollment. The Centers for Medicare and Medicaid Services (CMS) is now projecting private medical enrollment at 26 million by 2030.

A Growing Market in Health Care

If completed, the Humana acquisition would give Aetna the market share lead in a growing area of the health care market. There does not appear to be any single factor driving this unanticipated growth of Medicare Advantage. Many provider groups limit the number of CMS Medicare patients they take because CMS Medicare reimbursement flows through regional Medicare Administrative Contractors (MACs) – bureaucracies for which fraud discovery is a large part of the mission.

“The MACs are very bureaucratic and not easy to deal with, whereas commercial payers want market share and so provide relative good customer service to providers. Our billing department might have an issue with Humana, but when that happens at least we know we can get them on the phone” said a reimbursement director at a major east coast teaching hospital.

Medicare Advantage plan members enjoy extra benefits which can range from extra skilled nursing days to incontinence products to lower premiums. As managed plans private Medicare entails less provider choice than government Medicare, but as baby boomers become Medicare elligibles this may be less of an issue as they largely used to managed care.

For the payers there is a new financial incentive that somewhat compensates for the reduced payment rates – bonus payments for high-quality outcomes. Medicare Advantage exposes private payers’ financial performance directly to government policy which they can influence through lobbyist but not control or predict. Aetna’s bet on Medicare Advantage may well be a bet on managed care.

Tags: Growth Analytics, Healthcare & Life Sciences, Market Analysis, Payer, Provider